SDGs will be both an opportunity and a challenge in the years ahead. Several business organizations across the globe have started this journey by identifying and executing sustainable strategies as key drivers of their visions and business models. The SDGs present an opportunity for business-led solutions and technologies to be developed, and they offer an overarching framework to shape, guide, measure, and report the value created through business objectives, initiatives, and performance. Measuring and reporting on these goals enable business organizations to contribute to the SDGs while capitalizing on a range of benefits such as identifying future business opportunities and strengthening stakeholder engagement.

What are the Sustainable Development Goals? Where do they come from? Are companies ready to engage with them? How? What are the possible roles of management accountants in this space? We address (and perhaps answer) these questions by providing examples of a number of organizations—such as PepsiCo and Eni—that have been pioneering a certain degree of attention to the SDGs when measuring and reporting their business performances.

THE EVOLUTION OF SUSTAINABLE DEVELOPMENT

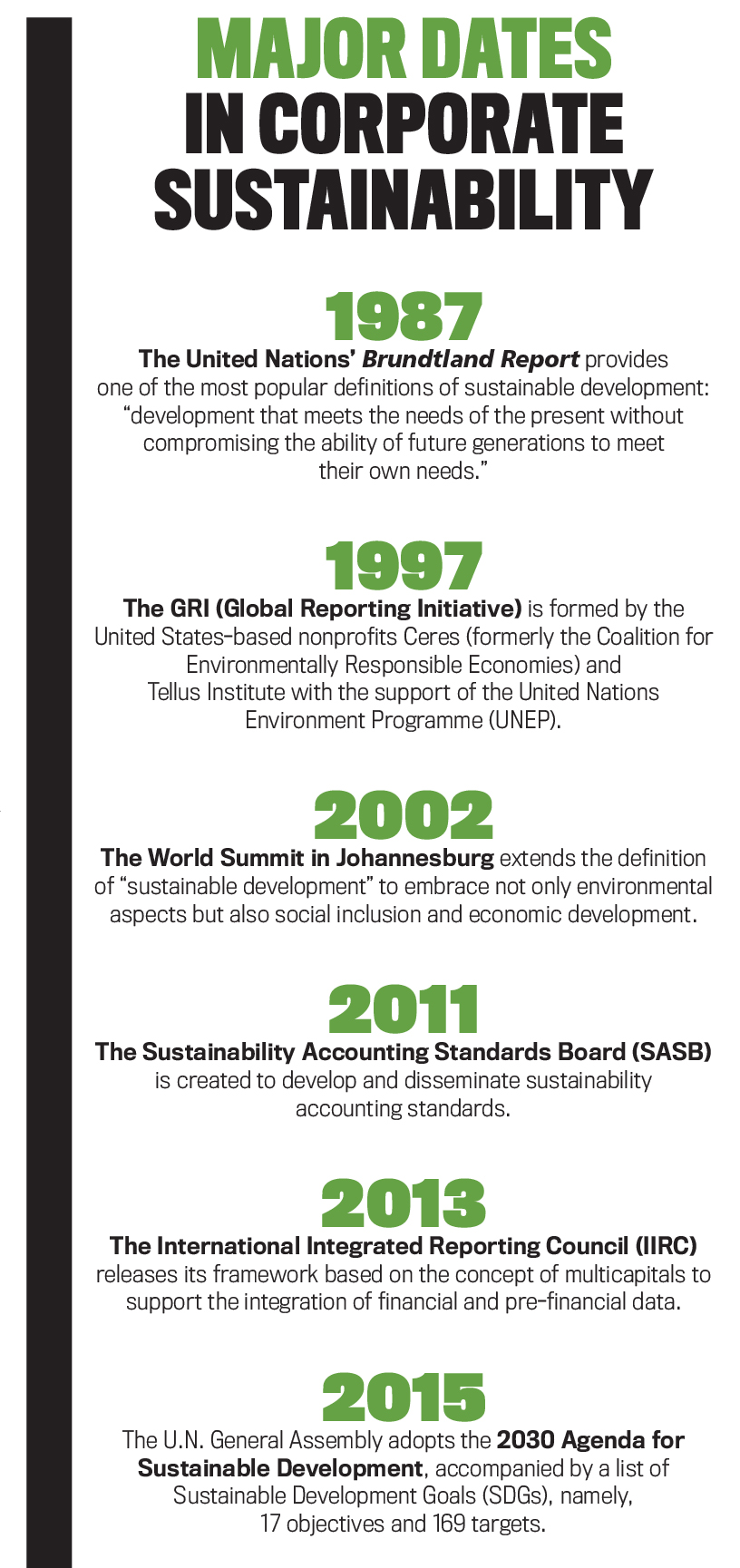

For the past 30 years or so, world leaders, supranational organizations, and national governments, as well as private and public organizations, have embraced sustainability as the cornerstone in their search for development and long-term growth. Sustainable development, conceptualized as the means to achieve sustainability, was defined in 1987 by the United Nations’ Brundtland Report as “development that meets the needs of the present without compromising the ability of future generations to meet their own needs.” Also known as Our Common Future, the report was the outcome of work by the World Commission on Environment and Development (WECD), which was sponsored by the U.N. and chaired by Norwegian Prime Minister Gro Harlem Bruntland.

In the years following the release of the Brundtland Report, various institutions and international bodies have further attempted to identify the core elements of sustainable development. With the intention to address the numerous issues broadly referred to as the domain of sustainable development (such as water emergency, health, climate change, pollution, social inequalities, access to energy, extreme poverty, and hunger), several major events and initiatives have taken place globally. For example, at the Johannesburg World Summit in 2002, sustainable development was defined as embracing social inclusion and economic development as well as environmental aspects.

In 2012, the U.N. further refined the concept of sustainable development (see U.N., “The Future We Want”), and in 2013 the United Nations Sustainable Development Solution Network (UNSDSN) extended it with the inclusion of good governance as a fourth pillar. In parallel, public, private, and nongovernmental organizations have been directly involved in the attempt to coordinate efforts regarding the sustainability agenda (see, e.g., the U.N. General Assembly resolution in 2010, “United Nations Millennium Declaration— General Assembly Resolution A/RES/55/2”). This process was consolidated in 2015 when the U.N. General Assembly adopted the 2030 Agenda for Sustainable Development, accompanied by a list of Sustainable Development Goals (17 objectives and 169 targets) that all countries of the world are encouraged to achieve by 2030. (See www.un.org/sustainabledevelopment.)

CREATING THE SUSTAINABLE DEVELOPMENT GOALS

The 21st Century started with a set of development goals known as Millennium Development Goals (MDGs). Designed for global action, the MDGs provided an important development framework between 2000 and 2015 and achieved success in several areas such as reducing poverty and improving health and education in developing countries. Gaining from the experience of MDGs, the U.N. decided to expand the goals to make them much wider, encompassing both developed and developing countries and expanding the challenges that must be addressed embracing a wide range of interconnected topics across the economic, social, and environmental dimensions of sustainable development.

This led to the identification and release of the SDGs, which were created by an inclusive process reflecting substantive input from all sectors of society and all parts of the world. The goals are applicable in developing and developed countries alike. Governments can translate them into national action plans, policies, and initiatives that reflect the different realities and capacities their countries possess. Different from the MDGs, the SDGs are designed to engage a wide range of organizations and shape priorities and aspirations for sustainable development efforts around a common framework. Most important, the SDGs recognize the key role that business organizations can play in achieving them. (See below for a summary of the SDGs.)

MAKING SDGS HAPPEN

Attempting to achieve the SDGs isn’t just a show of governmental and societal goodwill—it’s also a strategy increasingly made by proactive, sustainable organizations. Making SDG alignment part of their strategies and business models can help companies generate new revenue, increase supply chain resilience, recruit and retain talent, spawn investor interest, and assure license to operate. Such business organizations want to achieve the same ends as any other company by driving revenue growth, creating value, and accelerating business expansion. Critically, however, contributing to the SDGs through inclusive business models helps these organizations reinforce their awareness regarding the multiple and heterogeneous resources they use as well as the impact of the company’s activities on stakeholders.

The integration between sustainability initiatives and business goals can be comprehensive. Numerous successful companies have adopted this approach, steadily growing their bottom lines through innovation and adaptation while simultaneously stimulating progress toward the SDGs. In this article we’ll shed light on the early experiences of PepsiCo and Eni to illustrate how this process took place in two fundamental industries: (1) Food and Beverage and (2) Energy. Ultimately, these examples demonstrate how businesses’ growth and socioeconomic development can thrive together.

PEPSICO: GOVERNING SUSTAINABILITY THROUGH PERFORMANCE WITH PURPOSE

PepsiCo’s attention toward sustainable development received a boost in 2006 when the company launched its “Performance with Purpose” strategy, PepsiCo’s vision to deliver top-tier financial performance over the long term by integrating sustainability into business strategy. As shown in its 2015 Global Reporting Initiative Report and Performance with Purpose 2025 Agenda (www.pepsico.com/sustainability/Sustainability-Reporting), PepsiCo has centered Performance with Purpose work on Products (human sustainability), Planet (environmental sustainability), and People (talent sustainability). More recently, the company began closely mapping its Performance with Purpose plans to the SDGs (see Figure 1).

Click to enlarge.

PepsiCo put in place a strong sustainability governance as the foundation for delivering on the Performance with Purpose vision. Sustainability topics are integrated into, not separate from, the core business. PepsiCo’s Board considers sustainability issues an integral part of its business oversight. For example, as suggested by the 2015 GRI Report, “the Board addresses sustainability issues in its oversight of focus areas such as capital allocation, supply chain management, talent retention, and portfolio innovation” (see p. 7).

In 2015, after discussions with external stakeholders, the Board clarified its role with respect to sustainability by amending the company’s Corporate Governance Guidelines to add “sustainability” to the key aspects of PepsiCo’s business over which the Board has oversight responsibilities. In addition to full Board oversight of sustainability, the Board’s Nominating and Corporate Governance Committee was charged with annually reviewing PepsiCo’s key public policy issues, including its sustainability initiatives, and its engagement in the public policy process. PepsiCo’s sustainability governance structure reaches across the organization and focuses on three key areas whose successful development depends on management accounting and reporting practices:

- Governance and Decision Making. Accountabilities are assigned to individuals or teams to set strategy, prioritize activities, identify gaps, and facilitate decision making needed to advance the sustainability agenda.

- Tracking and Reporting Metrics (specific, measurable, time-bound targets). Where appropriate, metrics are defined and standardized for tracking progress against Performance with Purpose pillars. Additionally, reporting obligations are defined, and protocols are put in place to ensure compliance and data verification.

- Facilitating Business Integration. Each pillar has a sustainability agenda and has developed scorecards, checklists, and timelines focused specifically on measuring PepsiCo progress against its current targets.” (See pp. 7-8 of the 2015 GRI Report.)

Recently, as illustrated by the Report, PepsiCo reviewed the sustainability governance structure to identify opportunities to strengthen the integration of Performance with Purpose into its business agenda and processes. Going forward, the PepsiCo Executive Committee will assume direct oversight of the sustainability agenda, make strategic decisions, and champion performance management. Theme leads, empowered by the Executive Committee, will be appointed as subject matter experts to create and oversee global roadmap development and ensure business alignment to deliver on the goals. They are selected for their deep knowledge of the goals they are directing, and they work with teams composed of representatives from key functions across all geographic sectors (sector leads). Theme leads will align their agendas with the sector leads, who will be on point to ensure successful implementation of processes across businesses. Theme leads will be supported by the Sustainability Office, which will be responsible for driving the strategic framework and performance tracking.

Performance with Purpose allows PepsiCo to make valuable contributions to the SDGs. By focusing on creating and sustaining jobs, stimulating economic growth, transforming the product portfolio, protecting the planet, and enhancing the lives of people around the world, the company believes that impactful contributions to the SDGs will be made through its own business and its value chain (see p. 9 in the 2015 GRI Report). Additionally, the PepsiCo Foundation, which aligns with PepsiCo’s Performance with Purpose strategy and the SDGs, “aims to provide opportunities for improved health, environmental conservation, and education in underserved regions through sustainable development partnerships and programs.” (See p. 9 in the 2015 GRI Report.) All these are measures of PepsiCo’s success.

HOW ENI PURSUES THE SDGS

Like PepsiCo, the Italian energy giant Eni has invested time and resources in making sure that business strategies embody sustainability initiatives at their very core. For these reasons, over the last 10 years Eni has supported such a massive process of integration by innovating its management and accounting practices (see Cristiano Busco, Mark L. Frigo, Paolo Quattrone, and Angelo Riccaboni, “Redefining Corporate Accountability through Integrated Reporting,” Strategic Finance, August 2013, pp. 32-41). Now alignment with the SDGs seems a natural step in a process that’s rooted in making sustainability happen through inclusive strategies and business models.

Labelled as Eni for 2016, the company’s Sustainability Report (www.eni.com/en_IT/home.page) declares upfront how the 17 SDGs are used as a guide for project development over the long term. The report suggests how the private sector can, and must, play a crucial role as the engine of sustainable development over the long term, balancing global business and financial goals and local socioeconomic growth. This has led Eni to measure itself against the SDGs and reinforce the involvement in devising concrete solutions to move toward SDG achievement.

As a major operator in the energy field, Eni has two great challenges: maximizing access to energy and combatting climate change. To overcome these important challenges, Eni has defined a long-term integrated strategy to reconcile financial stability with social and environmental sustainability to create long-term value for all the stakeholders. To implement these strategic guidelines, Eni is leveraging three key levers (see Figure 2):

- A defined path to decarbonization;

- An operating model that reduces risks as well as environmental and social impacts; and

- A model with the hosting countries based on long-lasting partnership and cooperation.

First, Eni’s commitment in promoting a well-defined path to decarbonization lies mainly in reducing its activities’ emissions, developing renewable energies, and guaranteeing access to energy. With its plan to reduce greenhouse gas emissions, in 2016 Eni continued to reduce the emissions intensity index by 9% and is committed to continue to do so in order to reach the 43% reduction goal in 2025. The company will also continue to increase natural gas production, the bridge toward a low-carbon future, and to develop projects to install a capacity of 463 megawatts from renewables by 2020.

Second, to make access to new energy resources more efficient and minimize risks throughout the whole production cycle, Eni plans to conduct its business using an operating model of excellence aimed at safeguarding people and assets, respecting the environment, and engaging in research and development. Thanks to this model, over the last three years the company has registered Total Recordable Injury Rate (TRIR) values for both employees and contractors that were significantly lower than the peer average. In 2016, Eni reduced the TRIR by 20.8% compared with 2015, with the aim to reach zero injuries as the company continues investing in training to spread its safety-first culture.

Third, Eni’s cooperation model has been finalized to support local development, to minimize socioeconomic gaps, and to engage all the stakeholders. In this way, the company’s method of working aims at filling the gaps of local development and developing local resources for local growth. In the territories where Eni is present, the company doesn’t simply invest in the oil and gas production for export but mostly for the inland market while also investing in sectors that are distant from its own business, such as power stations to provide regional access to energy, promote local entrepreneurship, economic diversification, access to drinking water, and community health and education. For example, in Congo and Nigeria the company has invested $2 billion, providing about 60% and 20%, respectively, of the electricity of these two countries. This model soon will be repeated in Angola and Ghana.

MAKING SUSTAINABILITY A DRIVER OF THE BUSINESS MODEL

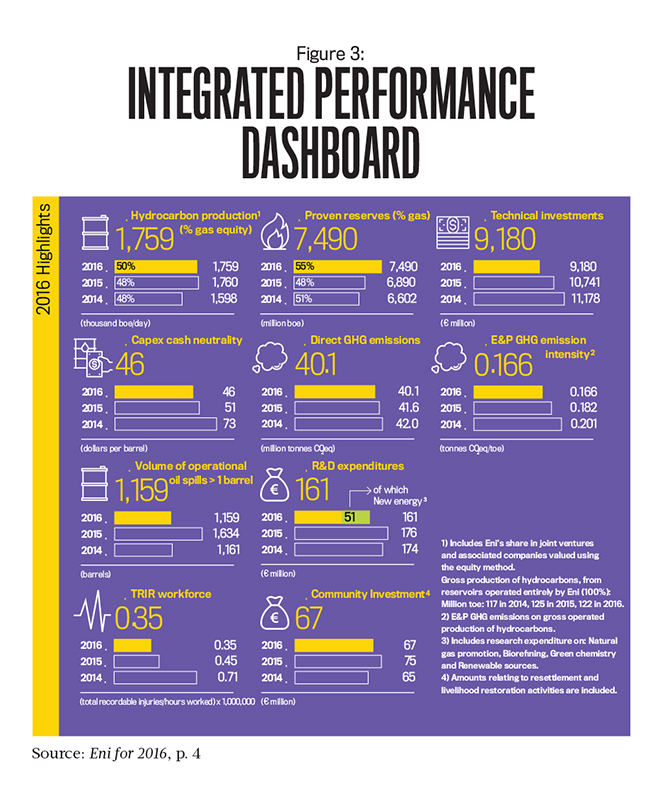

Eni’s contributions to the SDGs through the execution of inclusive business and holistic projects development build on a new way to look at performance measurement and reporting. With the intention of better understanding, communicating, and executing its business model and the strategy identified by the Board, over the last five years Eni has innovated its management and accounting systems by turning to integrated thinking and reporting. Championed by the vice president for sustainability and subsequently fully embraced by the Finance organization, the adoption of this emerging practice was carried out by a workgroup composed of managers from Finance, Sustainability, External Relations, Corporate Governance, and Integrated Risk Management. The main goal was to offer a comprehensive view of the process of value creation by monitoring and connecting those key financial and pre-financial performance(s) essential to sustain the execution of sustainable strategies. (See Figure 3 for an illustration of these integrated dashboards.)

Click to enlarge.

Eni’s approach to integrated thinking and reporting departed from a deeper understanding of the financial and operating objectives featuring the organization’s strategic plan and linked them with the resources used, the initiatives implemented, and the interdependencies among the various drivers at work. The purpose was to highlight the way in which initiatives of sustainability contributed to achieving the strategic targets of the company. An interesting example is offered by the Upstream division, where financial returns and exploration success were linked to operational excellence and innovation.

Eni’s performance measurement and reporting systems enable the company to monitor and measure the results achieved in the Upstream area by applying the Dual Exploration Model. If this model’s primary goal was to replace the existing reserves and, therefore, sustain organic production growth in the future through exploration, it makes it possible to immediately exploit certain discoveries and to generate cash flow through the sale of minority interests in some assets. This support in cash flow generated without compromising the goal of organically replacing the reserves at the same time reduces its financial exposure with regard to investments in the main projects.

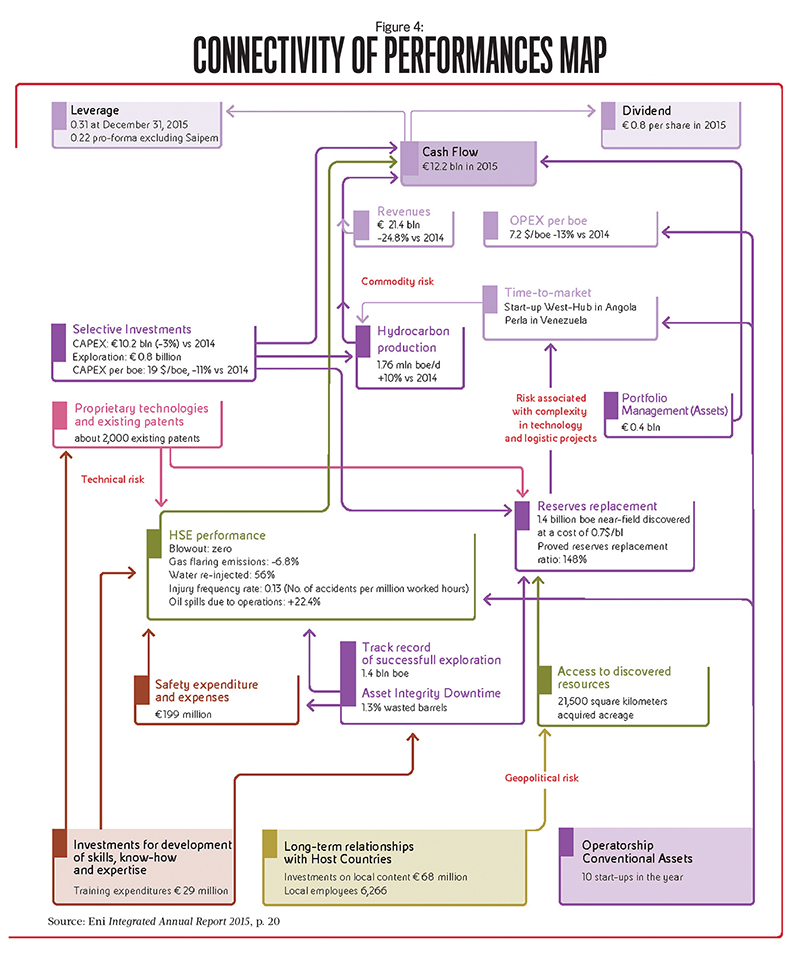

The holistic, integrated approach to measurement and reporting implemented by Eni permitted the company to highlight and value the key drivers of such a distinctive exploration strategy, which is based on a medium- to long-term vision; a focus on time to market; governance and management of exploration processes; professional development of Eni’s workforce; an ability to protect, disseminate, and renew know-how; a constant focus on the opportunities provided by technological innovation; and, finally, rigorous attention to Health, Safety, and Environmental (HSE) aspects. From a measurement and reporting point of view, Eni decided to capture the effects of specific actions and initiatives taken in the Upstream business and their impact on business objectives and risks in a cause-effect map showing a comprehensive connectivity of performances (see Figure 4).

Click to enlarge.

THE ROLE OF MANAGEMENT ACCOUNTANTS

As illustrated in the two company examples, the integration between sustainability initiatives and business goals is currently contributing to making SDGs happen in practice. The examples of PepsiCo and Eni show how this process is taking place as organizations strive to align competitiveness and sustainable growth. Because of their position and expertise, management accounting professionals have the potential to play a major role within this process.

Today, organizations operate in a complex and rapidly changing world characterized by a multitude of internal and external drivers, interdependencies, and trade-offs that influence the process of decision making, the promises that these decisions entail, and the expectations of a variety of stakeholders. Within this context, most organizations strive to balance competitiveness and sustainable growth by implementing programs and initiatives of sustainability that intend to achieve specific targets in terms of governance, social, and environmental impact. But isolated sustainability tactics don’t guarantee the achievement of sustainable performance(s), which instead requires an integrated approach to the planning, management, and reporting that must take into consideration how the interests and the contributions of a series of heterogeneous stakeholders are linked to the models for long-term value creation.

Management accounting professionals have a great opportunity to lead the process of making the SDGs happen and connect performance with purpose. Because of their financial expertise and positioning with organizations, they can contribute significantly to identifying, executing, and monitoring business decisions and strategies for long-term value creation. Management accounting offers tools and engagement platforms that can go beyond the representation of the initiatives of sustainability through a set of ad hoc targets and key performance indicators to include processes of mediation among the different stakeholders who are involved. In this area, management accountants and finance experts in general can lead the search for sustainable performance by suggesting pragmatic solutions that can monitor and communicate ways in which such an inclusive strategy and business models purpose may be converted into added value for a multitude of stakeholders.

Continuing research in the Center for Strategy, Execution and Valuation at DePaul University on sustainable high-performance companies suggests that business performance (including shareholder value creation) is an outcome of a company’s purpose of creating value for its customers as well as for employees, suppliers, and investors, which thereby can drive socioeconomic development and wealth creation (see Mark L. Frigo and Joel Litman, DRIVEN: Business Strategy, Human Actions and the Creation of Wealth, 2007). This research includes understanding how companies make the connection between innovation, customer value creation, and business performance. Companies studied, like Johnson & Johnson, have a clear understanding of the purpose of the firm and how it creates value through innovation: “value creation is driven by how the innovation will create value for patients, which, in turn, can create value for shareholders” (see Mark L. Frigo and Darren Snellgrove, “Why Innovation Should Be Every CFO’s Top Priority” Strategic Finance, October 2016, pp. 24-33). Connecting business success with socioeconomic development and taking care of future generations requires a clear understanding as to the meaning and context of maximizing long-term shareholder value. Recent research presented at the Center (see Bartley J. Madden, “The Purpose of the Firm, Valuation, and the Management of Intangibles,” Journal of Applied Corporate Finance, Spring 2017) suggests that maximizing shareholder value is best positioned as the result of a company achieving its purpose, not as the purpose of the company.

The measurement and internal/external reporting of sustainability strategies and performance by business organizations is an important issue for management accountants and financial professionals (see Tamara Bekefi and Marc Epstein, “21st Century Sustainability,” Strategic Finance, November 2016, pp. 28-37). For internal reporting it’s critical to integrate sustainability strategies and performance in planning, decision making, and monitoring activities. For external reporting, designing reports that are relevant and useful for a variety of stakeholders—including investors—is critical.

This is certainly the case for pioneer organizations such as PepsiCo and Eni, where the attempt to connect competitiveness and sustainable growth have been building on the cooperation between the finance experts and the sustainability function. This led to innovative planning, measurement, and reporting processes and practices, which have embodied inclusive strategies and business models designed to take advantage of the opportunities of the market and navigate through the challenges that such a comprehensive—but very much needed—approach presents. Overall, while making SDGs happen will be an opportunity and challenge for governments and business organizations in the years ahead, this process will rely on the skills and evolving expertise of management accounting professionals.

Sidebar: What Management Accountants Can Do to Implement SDGs

- Win board and senior management commitment on a selection of SDGs (focus only on those that the business organization can impact).

- Understand how key sustainability drivers and initiatives contribute to achieving business and financial strategies and goals.

- Integrate key sustainability drivers and the SDGs into the organization’s strategy and business model.

- Ensure that the SDGs and their connection with the organization’s strategy are understood cross-functionally in the business organization.

- Break down SDG targets and objectives for the organization as a whole into targets and objectives that are meaningful for individual subsidiaries, divisions, and departments.

- Make SDGs a central element of the process of planning, budgeting, and performance measurement, and include sustainability targets and objectives in performance appraisal.

- Connect SDGs and sustainability drivers with day-to-day decision making.

- Monitor and report sustainability initiatives and performance toward the SDGs in an integrated way.

September 2017