We’ve become increasingly reliant on getting information on contractors from Angie’s List or HomeAdvisor, and we want to know the rating of our Uber or Lyft driver. We’re used to rating everything from hotels to restaurants to movies, and companies use these subjective evaluations to improve the products and services they offer. But could subjective communication improve performance within a company? The short answer is “Yes.”

As a manager, you need to know the best way to get productivity out of your team. You need to motivate all of the team members to give their best effort. This is difficult, but, fortunately, research on team subjective communication (TSC) shows that managers can address these issues and increase productivity. Recent academic research by Markus Arnold from the University of Bern, R. Lynn Hannan from Tulane University, and Ivo D. Tafkov from Georgia State University can provide valuable guidance on some of the most vexing challenges with teams: improving the allocation of bonus pools among team members, reducing free riding, and improving team performance.

Arnold, Hannan, and Tafkov find that subjective communication from team members to a manager improves team member effort and performance, especially when team members have similar abilities. Subjective communication can be emails, memos, or rating systems like Yelp—any mechanism that the company or manager thinks would efficiently and effectively get the information from team members about their peers.

You would likely think it ridiculous if someone asked you, “Have you ever worked in a team or group?” Of course you have. We all have. Since you have been in a team, and you probably even managed at least one team, you’re undoubtedly familiar with the benefits and problems with teams. Teams are great for things like peer monitoring, information sharing, risk reduction, collaboration, and synergistic productivity. But many teams have free riders, people who just don’t pull their weight. This is one of the most frustrating parts of being a team member, and it’s one of the most vexing managerial issues: How can you get individual team members to be more motivated when they can hide behind team performance?

REDUCING FREE RIDING

Free riding is a problem because teams aren’t operating at their maximum potential if everyone isn’t working up to their ability. It can also demotivate other team members if they feel others are shirking. As managers, we can’t monitor individual performance in most teams directly with an objective performance measure, but one solution to the free rider problem could be TSC. This is a form of peer evaluation that’s conveyed to the manager by team members. It provides managers with information that can be used to reward individual team members and, therefore, reduce shirking.

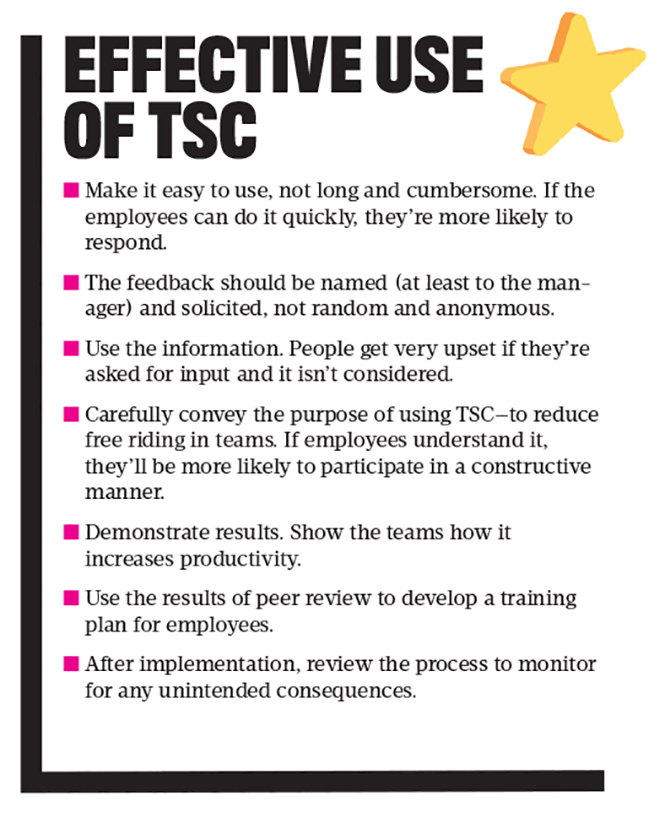

TSC can involve emails between team members and the boss, Google forms filled out with input on intrateam behavior and effort, rating systems like Yelp or Tripadvisor—tailored to your job—or other appropriate ways to give feedback on the team dynamics. The input from team members can be in the form of rating scales, percentages, or text descriptions of contributions. You want to make sure that the process doesn’t require too much time but also that it conveys the substance of what happened in the team. (See “Effective Use of TSC.”)

For example, think about a team that collects your receivables. While you have the objective, financial measure of dollars collected or the nonfinancial indicator of percent collected, how do you know who was working hard, making the calls, and facilitating the payments from your customers? If a particular employee hasn’t collected, was it because of a lack of effort or rather due to being given difficult customers? Without feedback, a free-riding employee can hide in the team performance. Allowing team members to communicate through TSC will increase their motivation and increase the value each team member adds to the organization.

BENEFITS OF TSC

To understand the value that this communication can provide, let’s take a quick look at the study that Arnold, et al., conducted. Published in The Accounting Review (see “Team Member Subjective Communication in Homogeneous and Heterogeneous Teams,” The Accounting Review, September 2018), their paper reports the results of an experiment with 148 students at Georgia State University. The participants were assigned to a role of either manager or one of three employees in a team. They stayed in the teams, with the same manager, throughout eight periods of the study. Each period, the employees chose their own effort levels and then learned their teammates’ effort levels, the translation of that effort to team output, total team output, and the team bonus pool. Just like in the real world, the higher the team effort, the higher the team output and the bonus pool.

The manager distributed the bonus pool to the team members, but the information that the manager had differed by experimental condition. In one condition the manager only knew total team output. In the TSC condition, however, employees submitted a recommendation to the manager for how to allocate the bonus pool between themselves and their two teammates. To induce effort in the experiment, participants were paid meaningful incentive compensation based on points earned.

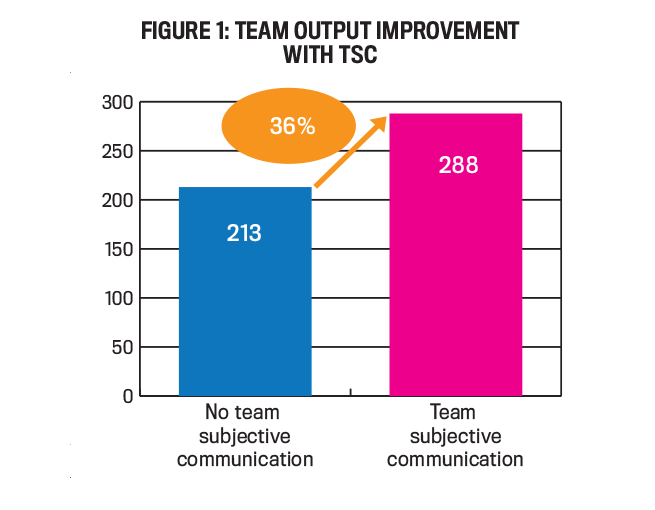

The research of Arnold, et al., shows that team output increases in the condition in which they provide TSC to the manager (see Figure 1). When TSC is allowed, productivity increases by 36%. The increase is both statistically and economically significant. Imagine how much your company could benefit from a 36% increase in productivity. If your team collecting receivables could increase collections by 36%, how would that affect your cash flow? Pretty nicely!

REAL-LIFE EXAMPLES

So, if this communication can increase team productivity in the lab, how can you get it in real life? Technology has enabled us to obtain subjective communication about many things. Companies are now putting in place TSC systems similar to the public ratings that we mentioned previously. For example, LivingSocial uses Rypple, which allows employees to post praise or criticism on peer work. According to a presentation by its director of global human resources, LivingSocial has been very successful in its implementation of Rypple, whereby 98% of eligible employees received peer reviews. It’s helping the company give feedback and rewards to employees for a job well done. It also gives clear information to help employees understand how and if they’re meeting goals and how to improve.

Amazon uses the Anytime Feedback Tool, allowing employees to send positive or negative feedback about peers to managers. While there was some initial backlash and negative publicity about this, Amazon made changes to improve the system. At first, employees felt overwhelmed with anonymous negative criticism. Amazon now has employees respond to questions and encourages positivity. In order to continue to improve the system and maximize the value available through real-time feedback, Amazon is considering eliminating the anonymity, sending unscreened feedback to the employee and enabling two-way communication.

Importantly, Amazon is relying primarily on unsolicited feedback, which tends to be negative. By seeking out solicited feedback (TSC), Amazon can reduce the imbalance of complaints and critiques by adding neutral and positive reports.

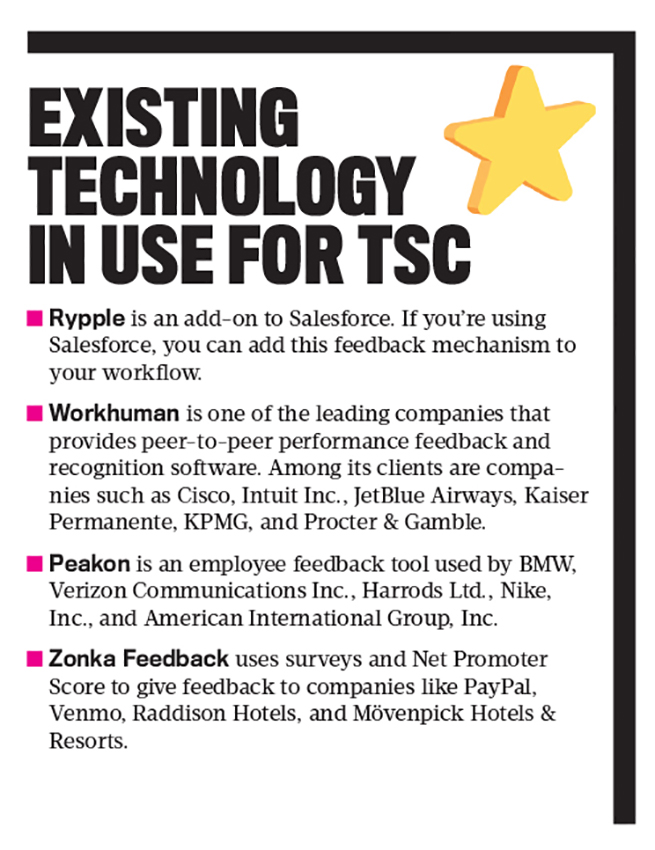

A third example we’ve seen is hotel and restaurant owners caring and responding to Yelp and Tripadvisor reviews. The same happens for employees and their peer TSC. To make this possible, the technologies can be easily added to current workflows to get subjective ratings from peers (see “Existing Technology in Use for TSC”).

TSC CHALLENGES

But what about the problems? In addition to the issues that Amazon experienced, certainly there are problems in asking for subjective ratings from peers. The primary problem is self-serving fairness bias. This is the tendency of individuals to mix together what is fair with what benefits themselves. Individual team members are apt to rate their own performance higher than that of their team members, especially when compensation and promotion are on the line.

Self-serving fairness bias causes a problem when there are multiple factors to use for assessing contributions. People naturally, even unconsciously, choose or place greater weight on those factors that will result in a higher personal contribution and, therefore, higher pay expectations. The self-serving fairness bias affects transfer pricing negotiations as well. For example, Steven J. Kachelmeier and Kristy L. Towry show that what is considered the fair transfer price depends on whether participants are assigned the role of buyer or seller, with the “fair” price perceived to be the one benefitting their assigned role (see “Negotiated Transfer Pricing: Is Fairness Easier Said than Done?” The Accounting Review, March 2002).

Arnold, Robert M. Gillenkirch, and Hannan show that market volatility makes it more difficult for buyers and sellers to negotiate a transfer price because uncertainty creates additional reference points for assessing a fair relative profit from the transfer (see “The Effect of Environmental Risk on the Efficiency of Negotiated Transfer Prices,” Contemporary Accounting Research, Summer 2019). Buyers focus on making sure the profits would be split fairly if the market price turns out to be low, so they want to pay a lower amount for the transfer as market volatility increases. Conversely, sellers focus on making sure the profits would be split fairly should the market price turn out to be high, so they want to charge a higher amount for the transfer as market volatility increases.

All that said, especially in teams that are ongoing, the incentives to overvalue one’s own contribution is mitigated. Team members know that other team members, with whom they continue to interact, will become aware of too much self-promotion. In addition, managers can be trained to look for this self-serving fairness bias—if one rating stands out from all the others, it’s probably off target and can be easily discounted. While self-serving fairness bias is a big problem that can’t be eliminated by experience or making employees aware of it, managers can be trained to watch out for the bias and take it into account in their allocations.

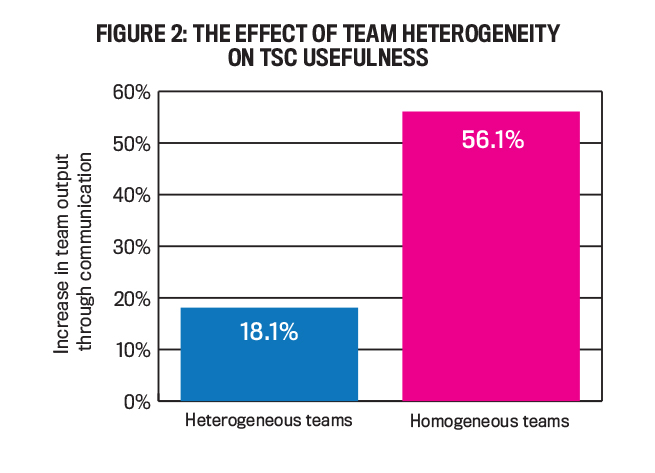

One other issue that might arise in the use of TSC is the lack of uniformity in teams. What if there’s a broad mix of skill sets in the teams? Can they evaluate each other fairly? Can an engineer evaluate the marketer in the team? The study by Arnold, Hannan, and Tafkov also addresses this issue. In their experiment, they randomly assign participants to be in homogeneous or heterogeneous teams. In homogeneous teams, individual team members have equal task-related abilities, and the effort of each individual contributes equally to team performance. In heterogeneous teams, individuals vary in ability, and the effort of each individual contributes in varying degrees to team performance.

There are two important results for heterogeneous vs. homogeneous teams. First, the ratings from different teams aren’t as clustered. If team members provide varied ratings, managers will have to spend more effort to process and use this information to allocate bonuses. If we think about our own experience with ratings, we don’t know what to think when someone rates a restaurant really highly and others say it’s the worst experience they’ve ever had, but if all the ratings are fairly clustered, we know it’s a reliable average rating.

Second, their results show that the improvement in performance from TSC is muted in heterogeneous teams. Although TSC does increase team output in heterogeneous teams (by 18.1%), the increase is much greater in homogeneous teams (56.1%), as shown in Figure 2. These results suggest TSC is valuable for the company even when teams are heterogeneous, just not as valuable as when the teams are homogeneous.

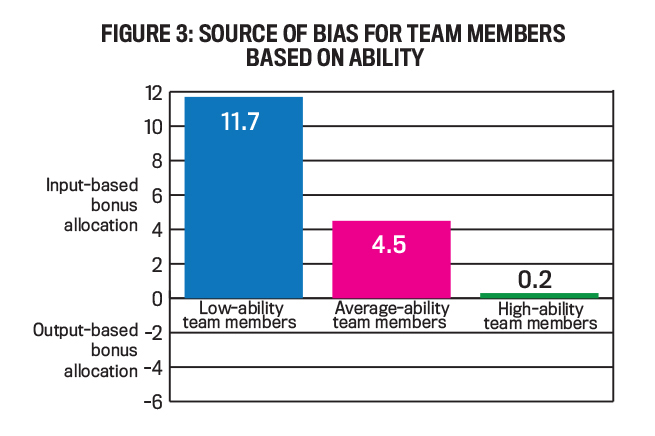

Interestingly, the spread in ratings in heterogeneous teams stems from differential notions of fairness. In the heterogeneous teams, one member is given “high ability,” one “low ability,” and one “average ability,” although these labels aren’t shared with participants. While low-ability team members tended to base their bonus allocations on input measures, which benefit them, high-ability team members tended to base their bonus allocations on output measures, which reward their efforts. Average-ability team members are about in the middle. This demonstrates self-serving fairness bias in action (see Figure 3).

TSC IN ACTION

Let’s translate this to practice. Consider a situation in which the finance department is setting up a dashboard to provide weekly financial visualizations to the managers in the company. There are six people working together on the task. They have six weeks to develop, test, and refine the product. They set goals, assign tasks to individuals, and proceed through the project. The team members have varying levels of experience with visualizations, interest in the task, and work ethic. At the end of the six weeks, they provide the controller with an excellent visualization. Their boss is thrilled and plans to reward them all for a job well done.

But despite the product being excellent, the team had some difficulty working together. One person had limited skills and didn’t try to use online help or get training. One team member thought the project was “stupid” and didn’t put in much effort. The four team members who were capable and interested in the task worked hard. They’re proud of their work, but they’ll be resentful if all members of the team receive equal praise, promotions, bonuses, or raises.

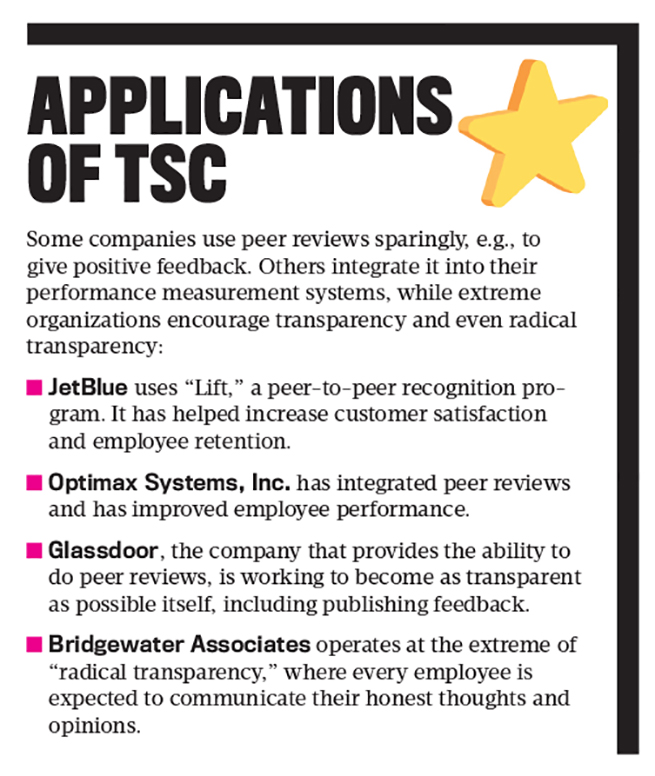

This is where TSC comes in. Since you, as manager, weren’t directly involved with the task, you don’t know these dynamics. Sending out a survey to the team and asking for input on the strengths and weaknesses of the team members can be very helpful in assigning the best people to the next important jobs, grooming stars for promotion, or for providing additional training and education for the team members who aren’t pulling their weight. Importantly, knowing that their performance is going to be reported on by their peers, team members are more willing to shoulder their fair share and to work toward the best collective outcome. Knowing who is contributing to the team allows you, the manager, to adjust. See “Applications of TSC” for examples of TSC being used in businesses today.

Getting good performance measurement requires more than just key performance indicators (KPIs). It requires understanding of the individual performance within the team. Research shows us that TSC can provide this understanding. While TSC can be a problem if the team members are so heterogeneous that they can’t properly judge each other’s contributions, TSC can prove beneficial in many environments. It can be quantitative surveys or descriptive text. Whatever the format, it’s essential to get input from your team.

December 2020